This is an effective tool for Customer Risk Profiling for lending – especially for the New to Credit customers or for those customers who have a bad Credit rating track (possibly because of COVID affecting livelihood)

The ability to pay is often measured using Credit Scoring models as standard credit practices. However, the expertise of knowing when and why people are honest will improve lending practices, be it for determining a transparent borrower profile or collections as a #gamechanger in realtime!

While every human responds to selective behavioral patterns, not everyone can access loans. If we begin our discussion from this simple understanding, the importance of using psychometrics along with lending principles combined as a fortified solution become self-explanatory.

ItP Q12 Framework (spelt: It-py)

The ItP Q12 framework borrows its name from ‘Intention to Pay’ where we pose 12 simple questions to assess borrower behavior behaviour logic across the 4 quadrants using a Survey methodology. The scores are recorded as interaction axioms stored as LMRS nodes for creating clusters to denote efficacy of behavior as part of Credit Risk modelling for; enhancing access to new markets lowering of Credit Risk and default creating borrower behavior profiles

Download the whitepaper here to read details .

Compared to Credit Rating scores, the ItP Q12 Decision Triad (AVOID < CAUTION < PROCEED) can further be utilised for;

How does the ideal borrower profile look?

The ideal borrower who would least likely default should have the above kind of scores;

High scores in R, Mid & High scores in L & M & Low scores in S

Combinations with L(Mid & Low), M(Low), R(High) & S(Low & Mid) shoot the del %age to 24.7%

The approach for an organisation can be multipolar or unidimensional; it could focus on lowering default by weeding out axioms which trigger any chance of default or focus on arriving at an optimum state where the loss of overall borrower profiles is adjusted to a focused delq %age.

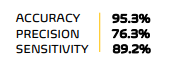

ACCURACY: Total Right decisions

PRECISION: Total AVOID decisions

SENSITIVITY: Accuracy for Total Positives

Have you been trying to find a fail-safe formula to lend to New to Credit customers ? And a tool to create credible Lending Profiles for customers? The Intention to Pay (ItP Q12) survey can be a good fit for your organisation.

To book a free trial reach us at score@pexitics.com / +91 734966 2320

Join us on LinkedIn : https://www.linkedin.com/company/pexitics.com/