Our ‘Intention to Pay’ ItP Q12 survey assesses customer intent for Loans. This is especially relevant now, as the ability to pay assessed through credit ratings have taken a dip post COVID and for New-to-Credit customers where a credit track is not available. ItP Q12 enables better Credit Risk Management and Risk segmentation.

ItP Q12 Framework (spelt: It-py) The ItP Q12 framework borrows its name from ‘Intention to Pay’ where we pose 12 simple questions to assess borrower behavior behaviour logic across the 4 quadrants: Law Abidance / Morality / Responsibility / Self Preservation – using a Survey methodology.

The scores are recorded as interaction axioms stored as LMRS nodes for creating clusters to denote efficacy of behavior as part of Credit Risk modelling for; enhancing access to new markets lowering of Credit Risk and default creating borrower behavior profiles

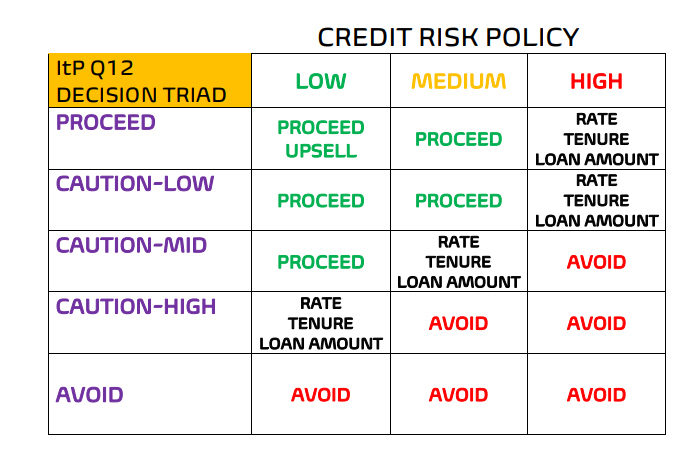

The ItP Decision Triad aims at supplementing the existing Credit lending policy for retail credit .

The ItP test simplifies the concept of Intention to Pay; it needs to be understood as an application from the concept of behaviorism compared to the scoring algorithm to determine ability profiling.